When you apply for a mortgage, lenders look at more than just your income and credit. They evaluate a combination of factors to determine whether you qualify and what loan terms you’ll receive. Outside of income and credit score, they will look at your debt-to-income ratio, assets, and how much you’re putting down. Another key metric they use is your loan-to-value ratio (LTV), a number that helps measure how much you’re borrowing compared to the value of the home.

It might sound technical, but it’s actually a simple concept. And once you understand it, you’ll have a much clearer picture of how your down payment affects your loan, your monthly payment, and even your interest rate.

At Homestead Financial Mortgage, we walk borrowers through this every day because LTV plays a role in nearly every mortgage decision.

What Is Loan-to-Value (LTV)?

Loan-to-value (LTV) is a percentage that compares how much you’re borrowing to the value of the home you’re buying.

Here’s the basic formula:

Loan Amount ÷ Home Value = LTV

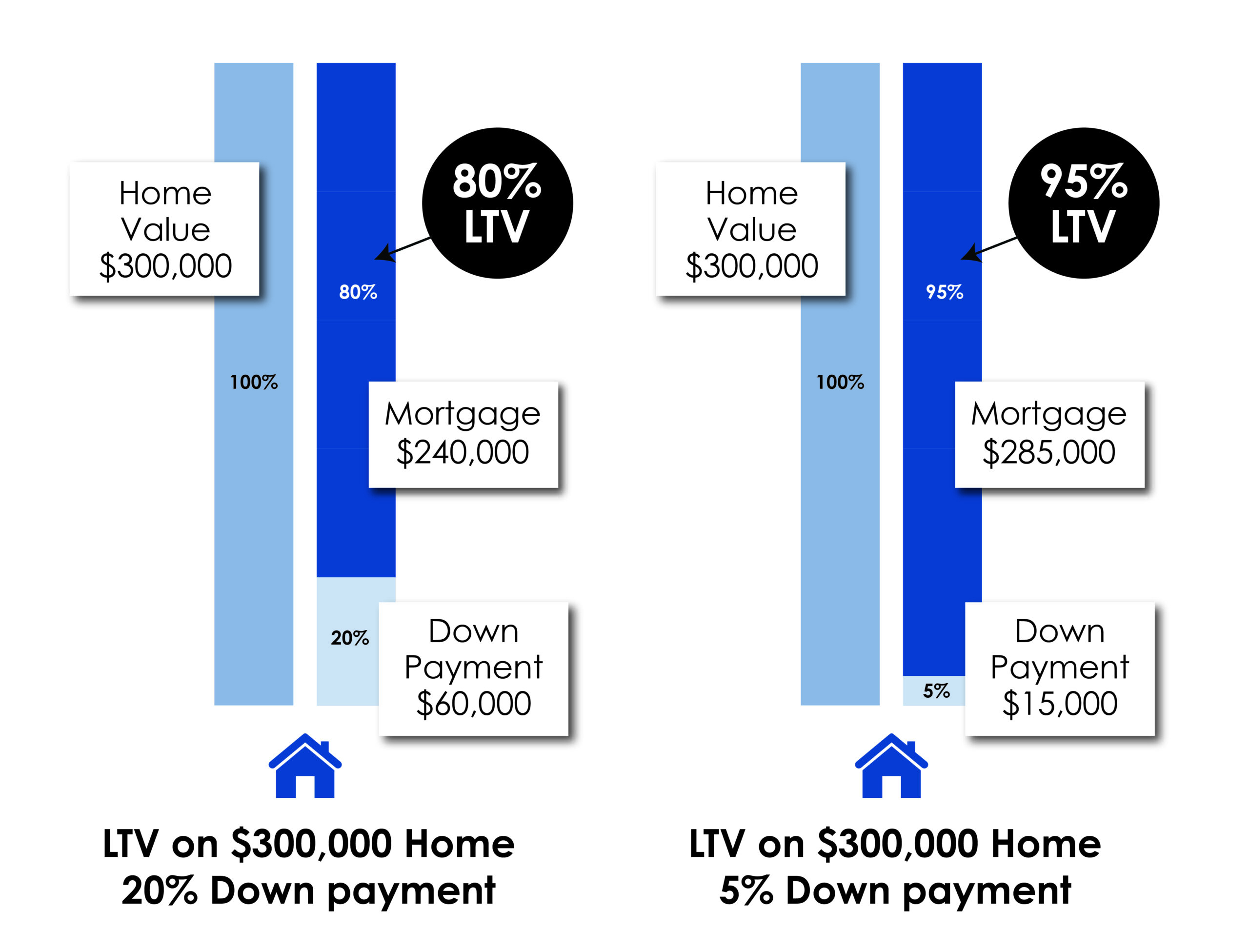

Example:

- Home price: $300,000

- Down payment: $60,000

- Loan amount: $240,000

$240,000 ÷ $300,000 = 80% LTV

So, in this case, your LTV would be 80%.

Why LTV Matters

LTV is one of the primary ways lenders measure risk. A higher LTV means you’re borrowing a larger percentage of the home’s value, which leaves you with less equity upfront and increases the lender’s risk. On the other hand, a lower LTV means you’ve invested more into the home at the start, which reduces that risk. Because of this, your LTV can directly impact several parts of your mortgage, including whether you’re approved, the interest rate you’re offered, and whether you’ll need to pay for mortgage insurance.

How Your Down Payment Affects LTV

Your down payment and your LTV are directly connected.

- Higher down payment = Lower LTV

- Lower down payment = Higher LTV

Here’s how that typically looks:

- 20% down → 80% LTV

- 10% down → 90% LTV

- 5% down → 95% LTV

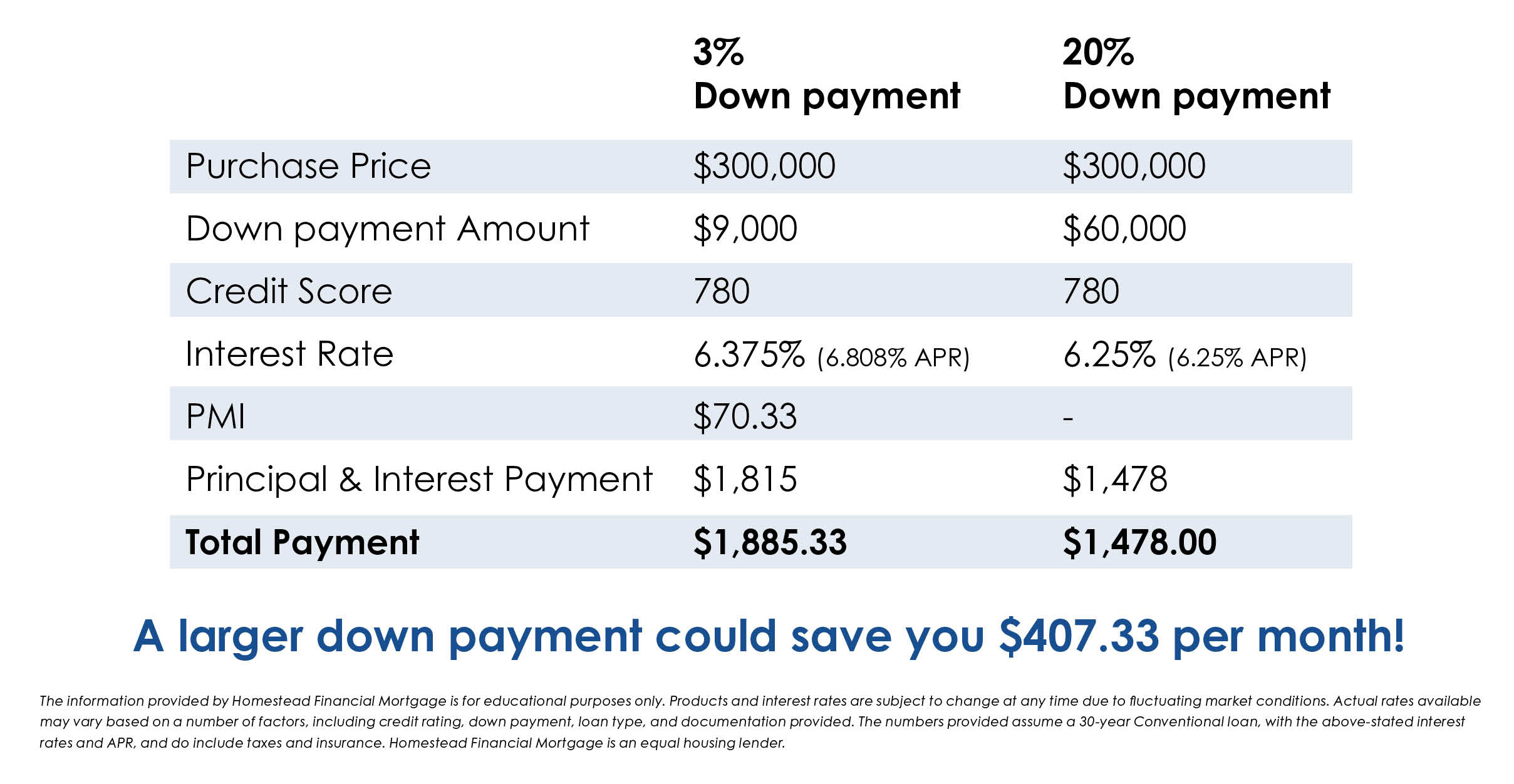

Even small changes in your down payment can shift your LTV, which can affect your loan terms, such as your interest rate and whether you have PMI, and ultimately affect your monthly loan payment. So, while needing a 20% down payment is a common misconception, the amount you put down can affect the terms of your loan.

LTV and Mortgage Insurance (PMI)

One of the biggest reasons LTV matters is because of private mortgage insurance (PMI). For most Conventional loans, if your LTV is above 80%, PMI is typically required, while an LTV of 80% or lower usually allows you to avoid it. PMI protects the lender, not the borrower, but it does add to your monthly payment. The good news is that PMI isn’t always permanent; in many cases, it can be removed once your LTV reaches 80%, either by paying down your loan or through an increase in your home’s value.

LTV and Interest Rates

LTV can also affect the interest rate you’re offered.

In general:

- Lower LTV = better (lower) interest rates

- Higher LTV = slightly higher rates

This is because lower LTV loans are seen as less risky.

Even a small difference in rate can have a noticeable impact on your monthly payment over time. You’ll have noticed in our graphic above, discussing down payment amounts, that there’s a difference in interest rates between the two down payment amounts when all other factors are the same.

What Is Considered a “Good” LTV?

There isn’t a single “perfect” LTV; it depends on the type of loan and your overall financial situation.

Here are some general guidelines:

- 80% LTV or lower

- Ideal for Conventional loans

- Avoids PMI

- 80%–95% LTV

- Common for Conventional loans with smaller down payments

- PMI typically required

- 96.5% LTV (FHA loans)

- Designed for lower down payments (as little as 3.5%)

- Up to 100% LTV (VA/USDA loans)

- Available for qualified borrowers

- No down payment required

How Loan-to-Value (LTV) Affects Refinancing

Loan-to-value plays a key role when you refinance your mortgage, but it becomes especially important with cash-out refinances. In a standard rate-and-term refinance, a lower LTV can help you qualify for better interest rates and may allow you to eliminate mortgage insurance. With a cash-out refinance, however, LTV directly determines how much equity you can access.

Most lenders set limits on how much you can borrow, often capping cash-out loans at around 80% of your home’s value, meaning you need to maintain a certain amount of equity after the refinance. If your LTV is too high, your options may be limited or come with higher costs. Because of this, understanding your home’s value and your current loan balance is essential when deciding whether a refinance makes sense for your goals.

Final Thoughts

Loan-to-value may seem like just another number, but it plays an important role in how your mortgage is structured. It influences how much you’ll need for a down payment, whether you’ll be required to pay mortgage insurance, and the rate and overall terms you’re offered.

Understanding the basics of what goes into mortgage approval, including your LTV and how to adjust it, can help you make more informed decisions when buying a home.

At Homestead Financial Mortgage, we help you look at the full picture and find the right balance between down payment, monthly payment, and long-term goals. If you’re ready to buy a home or are ready to refinance, reach out today to learn more about what you qualify for.