Building credit is an essential financial milestone whether you’re just starting out or looking to rebuild after financial setbacks. A secured credit card is one of the most effective tools for establishing or improving your credit. Unlike traditional credit cards, secured cards require a security deposit, making them accessible even to those with no credit or poor credit histories. We’ll break down what a secured credit card is and how to utilize it to build your credit score.

What is a Secured Credit Card?

A secured credit card functions like a traditional credit card but requires a cash deposit upfront. This deposit typically acts as your credit limit. For example, if you deposit $500, your credit limit will generally be $500. The deposit reduces the lender’s risk, making secured cards easier to obtain for those with less-than-stellar credit.

What is the point of a Secured Credit Card?

Credit scores are made up of many factors. Payment history, credit length history, and the amount owed are just a few examples. You will need a strong credit score to obtain loans. A good score typically signals that you are a good borrower, which means you will also get better offers of rates and terms. Life happens, though, and sometimes credit can get a bit turned upside down. Or you could also just be starting out on your credit journey and need to establish a credit history. This is where a secured card can come in handy. Getting approved for a secured card is easy, and it can help you get your credit on the right track.

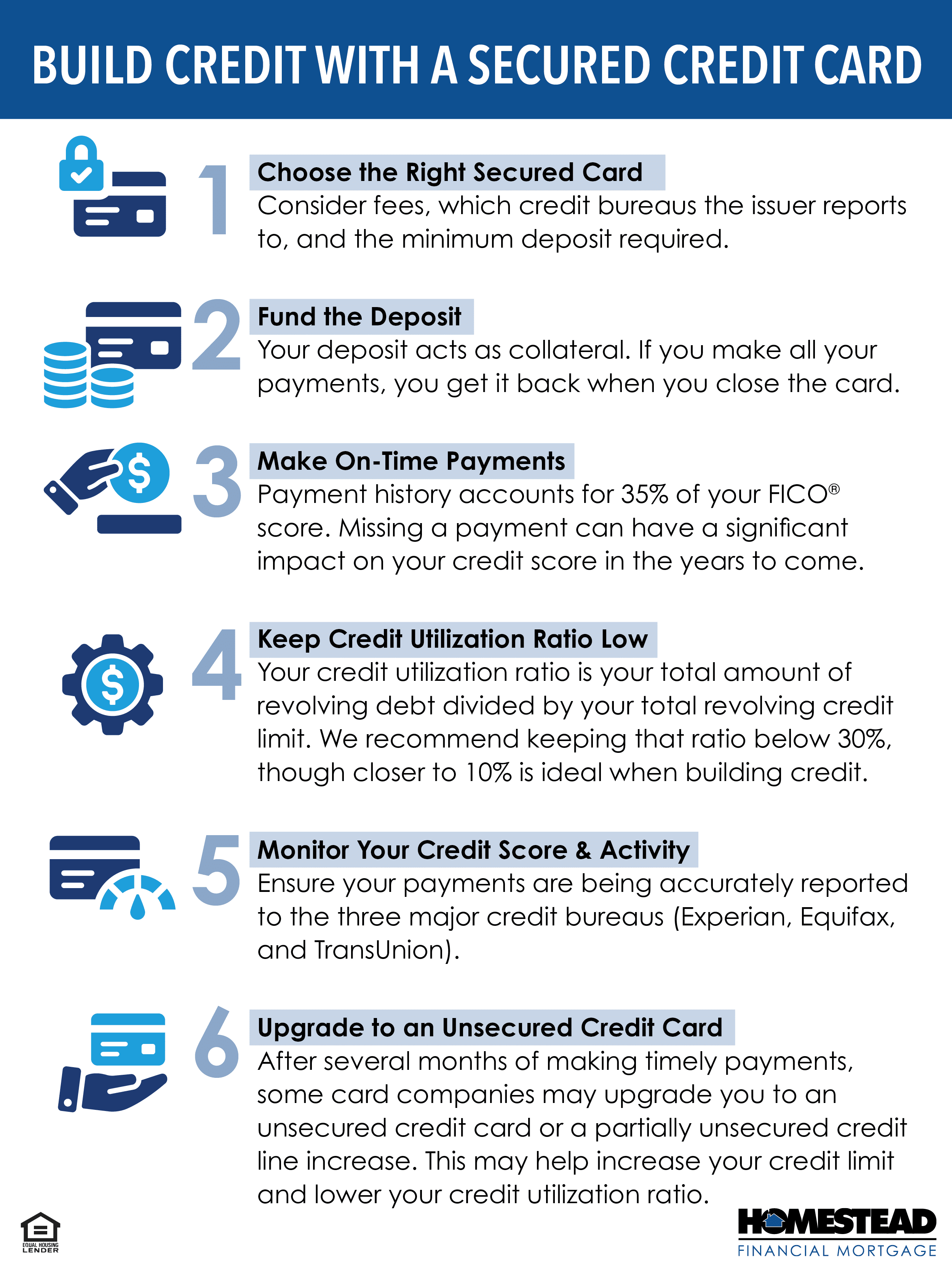

Step 1: Choose the Right Secured Credit Card

Not all secured credit cards are created equal, so choosing one that best fits your needs is essential. Consider the following when selecting a card:

- Low Fees: Look for a card with minimal annual fees and no hidden charges.

- Reports to All Three Credit Bureaus: Ensure the card issuer reports your activity to the three major credit bureaus (Experian, TransUnion, and Equifax). This is crucial for building your credit score.

- Reasonable Interest Rates: While secured cards typically have higher interest rates than unsecured cards, shop around for the lowest possible APR.

- Upgrade Path: Some secured cards allow you to transition to an unsecured card after a period of responsible use. This can be a great way to continue building credit.

A couple of options we have previously recommended are through Discover and Captial One. Another tool that our lenders use is OpenSky. This is a helpful, low-cost option to boost your scores within just a few weeks.

Step 2: Make Your Deposit and Use the Card Wisely

Once you’ve chosen a secured credit card, you’ll need to make a deposit. The amount deposited often dictates your credit limit, so choose an amount you’re comfortable with. After that, it’s time to use your card wisely:

- Make Small Purchases: Use the card for small, manageable purchases like groceries or gas. This keeps your credit utilization low, which benefits your credit score.

- Pay In Full and On Time: Always pay off your total balance each month to avoid interest charges. Consistent on-time payments are among the most important factors in building your credit.

Step 3: Monitor Your Credit Utilization Ratio

Your credit utilization ratio is the percentage of your available credit that you’re using. For example, if your credit limit is $500 and you have a balance of $100, your credit utilization is 20%. Keeping your utilization below 30% is recommended to impact your credit score positively.

Step 4: Check Your Credit Reports Regularly

Monitoring your credit reports from all three bureaus is essential. You’re entitled to a free credit report from each bureau once a year through AnnualCreditReport.com. Checking your reports regularly allows you to:

- Track Your Progress: See how your responsible use of a secured credit card is improving your credit score.

- Identify Errors: Mistakes on your credit report can hurt your score. If you find any errors, dispute them promptly with the credit bureau.

Step 5: Transition to an Unsecured Credit Card

After six to twelve months of responsible use, you should start to see some improvement in your credit score. Some secured cards offer an upgrade to an unsecured card, which doesn’t require a deposit and often comes with better terms. If your card doesn’t offer this option, consider applying for a new, unsecured card with better benefits.

Benefits of Using a Secured Credit Card

- Builds credit—we often see 30-50 point improvements.

- Registration doesn’t require a hard credit pull.

- The deposit is fully refundable.

- Learn to manage credit responsibly.

- Provides a smoother transition to an unsecured credit card when ready.

- You can check your Credit Karma account to see when the new account is posted and review your scores.

Building credit with a secured credit card is a gradual process, but with patience and discipline, it’s an effective way to establish or rebuild your credit. By choosing the right card, using it responsibly, and keeping an eye on your credit utilization and reports, you can steadily increase your credit score and gain access to better financial opportunities in the future.