According to the National Association of Realtors, the average age of first-time homebuyers reached an all-time high of 38 in 2024, up from 29 just 15 years ago. Rising home prices, student debt, and slower wage growth have delayed homeownership for younger generations. Many also prioritize career advancement, travel, or education before buying a home. The shortage of affordable housing has further pushed this milestone into later adulthood.

We’ll discuss common barriers to homeownership and strategies to overcome them.

Newly Employed College Graduates Can Buy a Home

A common misconception is that recent graduates can’t buy a home due to income, credit history, or savings constraints. However, lenders often accept a diploma as proof of employment history and consider future income when assessing eligibility. While challenges like student debt or credit scores exist, solutions such as co-signers, secured credit cards, and specialized mortgage programs can help.

Competitive Market & Rising Home Prices

Despite high mortgage rates, home prices continue to climb due to supply shortages. Inflation, construction costs, and slow adoption of new building technologies contribute to this imbalance. While prices may not stabilize soon, there are ways for buyers to navigate the market.

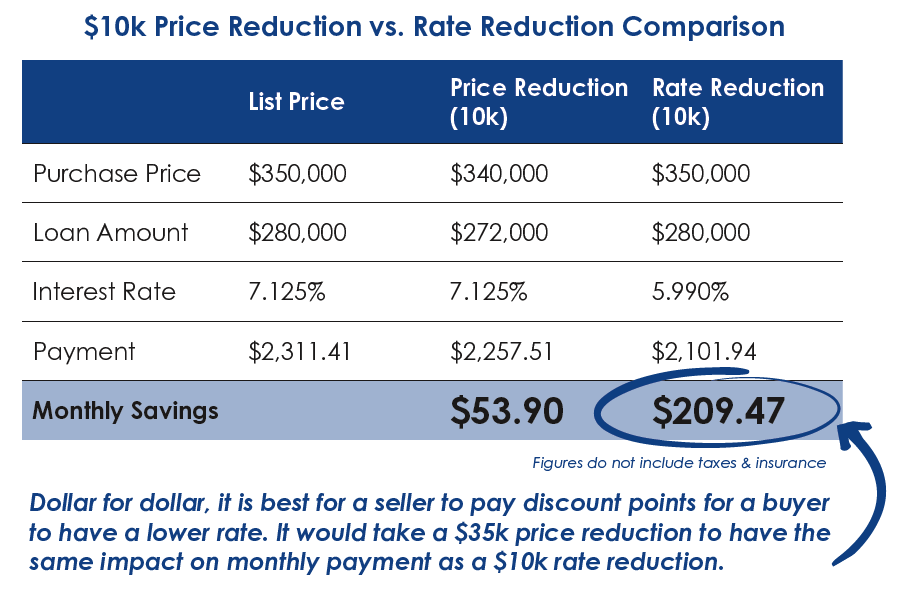

Negotiate for a Rate Buy-Down vs. Price Reduction

Rising rates have increased housing inventory by 10-20%, leading to negotiation opportunities. However, instead of focusing on price reductions, buyers may benefit more from negotiating a rate buy-down, which lowers monthly payments significantly.

Comparison is based on a 701 credit score, 20% down payment, 30-year term, 7.125% interest rate with an APR of 7.238%, and a 5.990% interest rate with an APR of 6.362%. The information provided by Homestead Financial Mortgage is for educational purposes only. Products and interest rates are subject to change at any time due to fluctuating market conditions. Actual rates available may vary based on a number of factors, including credit score, down payment, loan type, and documentation provided.

Buy a Home with Another Person

Co-buying with a friend or family member can make homeownership more affordable. By pooling resources, buyers can qualify for larger loans and share financial responsibilities. However, clear legal agreements should outline ownership, financial obligations, and exit strategies.

House Hacking

House hacking involves renting out part of your home—such as extra bedrooms, multi-family units, or short-term rentals—to offset mortgage costs. Financing options like FHA, VA, and conventional loans make this strategy accessible, particularly for first-time buyers. Success depends on careful property selection, tenant screening, and an understanding of local rental laws.

Down Payment Assistance Programs

State and local programs offer grants, forgivable loans, or low-interest loans to help with down payments and closing costs. For example, Illinois’ SmartBuy Program provides down payment assistance and helps pay off student loan debt, making homeownership more feasible for those burdened by education loans.

By leveraging such programs, first-time buyers can achieve their dream of owning a home more affordably while addressing other financial challenges. We break down some options that can help buyers get down payment assistance in Illinois, Missouri, Kansas, and Texas.

Marry the House, Date the Rate

With rent increasing by 15-20% in recent years, homeownership can be a more stable financial choice. Renting means paying 100% of someone else’s mortgage, while buying allows you to build equity. Interest rates fluctuate over time, meaning homeowners can refinance when rates drop, unlike renters who face ongoing increases. . That’s why we like to say Marry the House, Date the Rate.

Buying a House is an Investment

Homeownership builds wealth in two ways: paying down the mortgage increases equity, and property values typically appreciate over time. Historically, home values rise by an average of 4% per year, helping homeowners build long-term financial stability.

Despite today’s challenges—rising home prices, mortgage rates, and economic uncertainty—owning a home remains one of the most effective ways to build wealth. As a lender, we are committed to helping buyers navigate these obstacles with tailored solutions, including down payment assistance programs, flexible loan options, and expert guidance. Together, we can create a plan to help you achieve homeownership and long-term financial growth.