Written by:

Jayson Hardie – Chief Executive Officer- (636) 256-5712

Jayson Hardie – Chief Executive Officer- (636) 256-5712

When interest rates start rising, buyers begin looking for ways to reduce their monthly payment. And understandably so, since even small changes in mortgage rates can have a major impact on affordability.

Historically, 30-year fixed mortgage rates in the U.S. have averaged around 7%–8% over the last 50+ years. Freddie Mac’s long-running mortgage survey shows the historical average since 1971 is roughly 7.7%. So, while today’s rates may feel high compared to the record lows we saw during COVID, they’re actually much closer to long-term historical norms.

The challenge is that today’s buyers are dealing with both higher rates and higher home prices, which puts even more pressure on monthly payments.

And when buyers start shopping and negotiating, the default strategy is usually simple:

Lower the price.

It feels logical. It feels straightforward. And for years, that’s how many deals got done.

But in today’s market, lowering the purchase price is often the least effective way to improve affordability.

If the goal is to create the biggest impact on a buyer’s monthly payment, there’s usually a much better option:

Use seller concessions to buy down the buyer’s interest rate instead of reducing the contract price. The difference in monthly payments using this strategy is significant.

Why Rate Buydowns Create More Buying Power

Let’s say a buyer is shopping for a $350,000 home but needs to keep their monthly payment in a comfortable range of about $1,200.

Without lowering the interest rate in today’s market, the seller may need to reduce the purchase price by roughly $30,000–$35,000 just to create a payment the buyer can comfortably afford.

That’s a substantial price reduction and one that a seller is not likely to consider.

But instead of cutting the home price that dramatically, the seller could use a much smaller concession toward a rate buydown instead.

In many cases, a seller’s contribution of around $10,000 toward lowering the buyer’s rate can create a similar impact on the monthly payment while allowing the seller to keep the contract price much stronger.

That’s why more buyers and sellers are looking beyond simple price cuts and focusing on financing strategies that improve affordability more efficiently.

Real-World Comparison: Price Reduction vs. Rate Buydown

Let’s look at a side-by-side example using numbers buyers and sellers are seeing in today’s market.

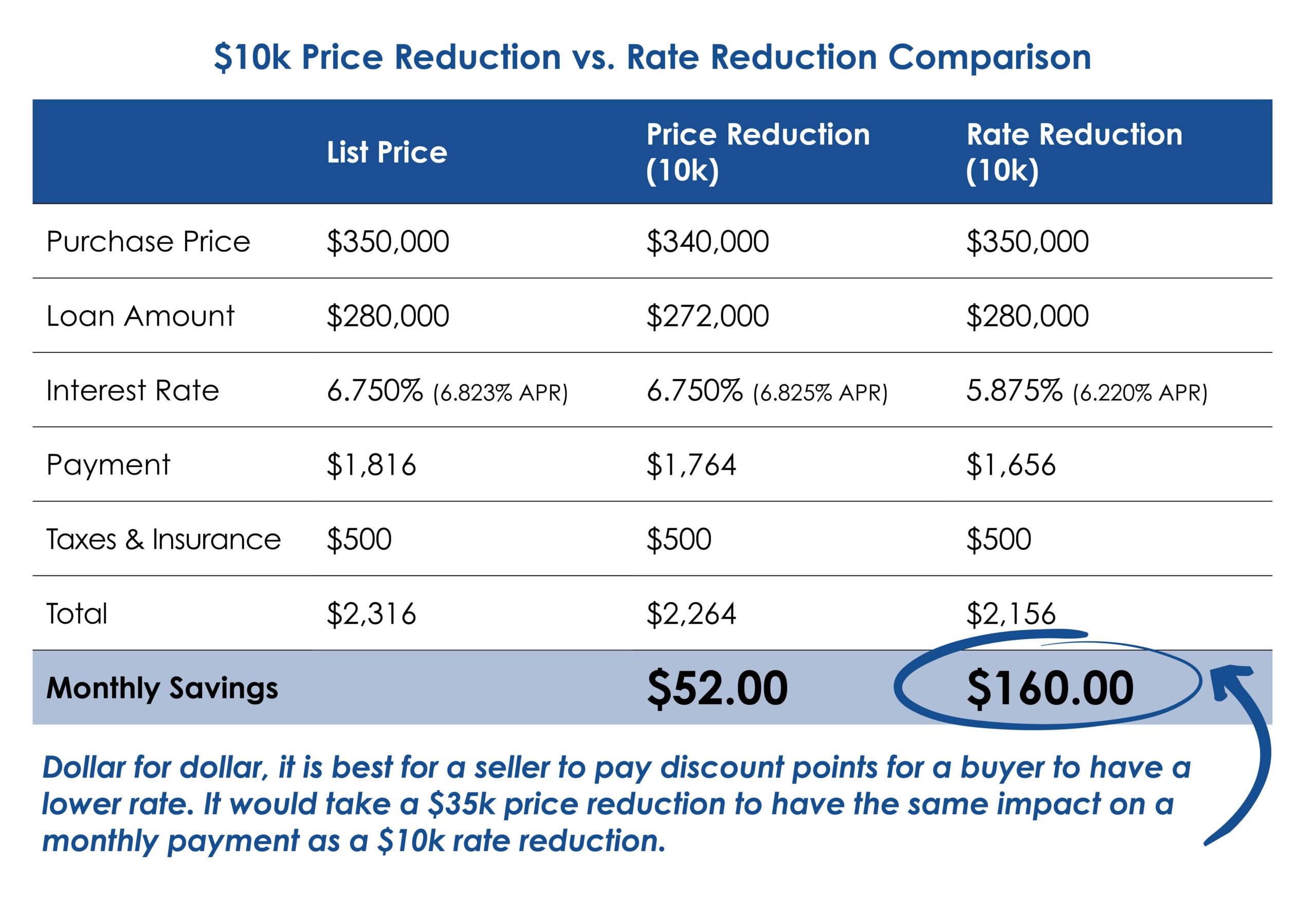

Comparison is based on a 780 credit score, a 20% down payment, and a Conventional loan with a 30-year term. 360 monthly payments of $1,816, $1,764 & $1,656. Fixed-rate mortgage. Subject to credit approval. The information provided by Homestead Financial Mortgage is for educational purposes only and is not a commitment to lend. These figures are an estimation and may not reflect the exact terms of your loan. Products and interest rates are subject to change at any time due to fluctuating market conditions. Actual rates may vary based on factors such as credit score, down payment, loan type, and documentation provided.

Scenario 1: $10,000 Price Reduction

- Purchase Price: $350,000 → $340,000

- Loan Amount (20% down): $272,000

- Interest Rate: 6.750%

- Monthly Payment: $2,264

Monthly Savings: $52.00

Scenario 2: $10,000 Seller-Paid Rate Buydown

- Purchase Price: $350,000

- Loan Amount (20% down): $280,000

- Interest Rate: 5.875%

- Monthly Payment: $2,156

Monthly Savings: $160.00

Same $10,000 from the seller.

But the rate buydown creates nearly three times the monthly payment savings compared to the price reduction. That’s the entire point.

When a buyer is financing a home purchase, interest rate reductions typically create a much larger affordability benefit than small price cuts.

Why This Strategy Matters More in Today’s Market

When mortgage rates were in the 3% range, price reductions carried more weight because borrowing money was inexpensive.

Today, affordability is driven much more by the interest rate than by small movements in purchase price.

Buyers have become increasingly payment-sensitive, and sellers are more open to offering concessions to keep transactions moving. That’s why many successful negotiations today are shifting away from:

“How much can we lower the price?”

And more toward:

“How can we structure the financing to create the best monthly payment?”

Why It’s a Win for Both Buyers and Sellerss

For buyers, a lower interest rate can mean:

- Lower monthly payments

- Improved affordability

- Easier loan qualification

- Better monthly cash flow

- Less interest paid over time

For sellers, a rate buydown can help:

- Preserve the contract price

- Protect neighborhood comps and appraised values

- Reduce the need for large price cuts

- Make the home more attractive to buyers

- Increase the likelihood of getting the deal closed

It’s one of the few negotiation strategies that can genuinely benefit both sides of the transaction.

The Bottom Line

If you’re buying a home in today’s market, focusing only on the purchase price may not be the smartest financial move. Sometimes, the better strategy is negotiating how the seller’s concessions are used.

Because when affordability is the goal, lowering the interest rate often has a much bigger impact than lowering the price.

In many cases, that difference can save buyers hundreds of dollars per month while helping sellers avoid unnecessary price reductions.

That’s not just smart negotiating. That’s smart financing. Our Homestead Loan Advisors are here to walk you through every step and get you into the home of your dreams at a payment you can afford.