Why Waiting Could Cost More Than You Think

If you’ve been thinking about buying a home, you’re probably asking the same question many buyers have asked:

“Should I buy now, or wait for mortgage rates to come down?”

It’s understandable. Over the past several years, rising mortgage rates and higher costs across the board have made home affordability a significant concern for many prospective buyers.

But while most buyers are focused on interest rates, they often overlook another factor that can have an even bigger impact on their long-term financial picture: home prices.

While today’s mortgage rates may feel high compared to the record lows we saw in 2020 and 2021, they’re actually much closer to the historical average Americans have experienced over the past 50 years. In other words, today’s rates aren’t unusually high; they’re more in line with what many homebuyers have considered normal throughout history.

That’s important to remember because mortgage rates are constantly changing. They rise, they fall, and they rise again. Trying to perfectly time interest rates can be difficult, if not nearly impossible, given how often mortgage rates change.

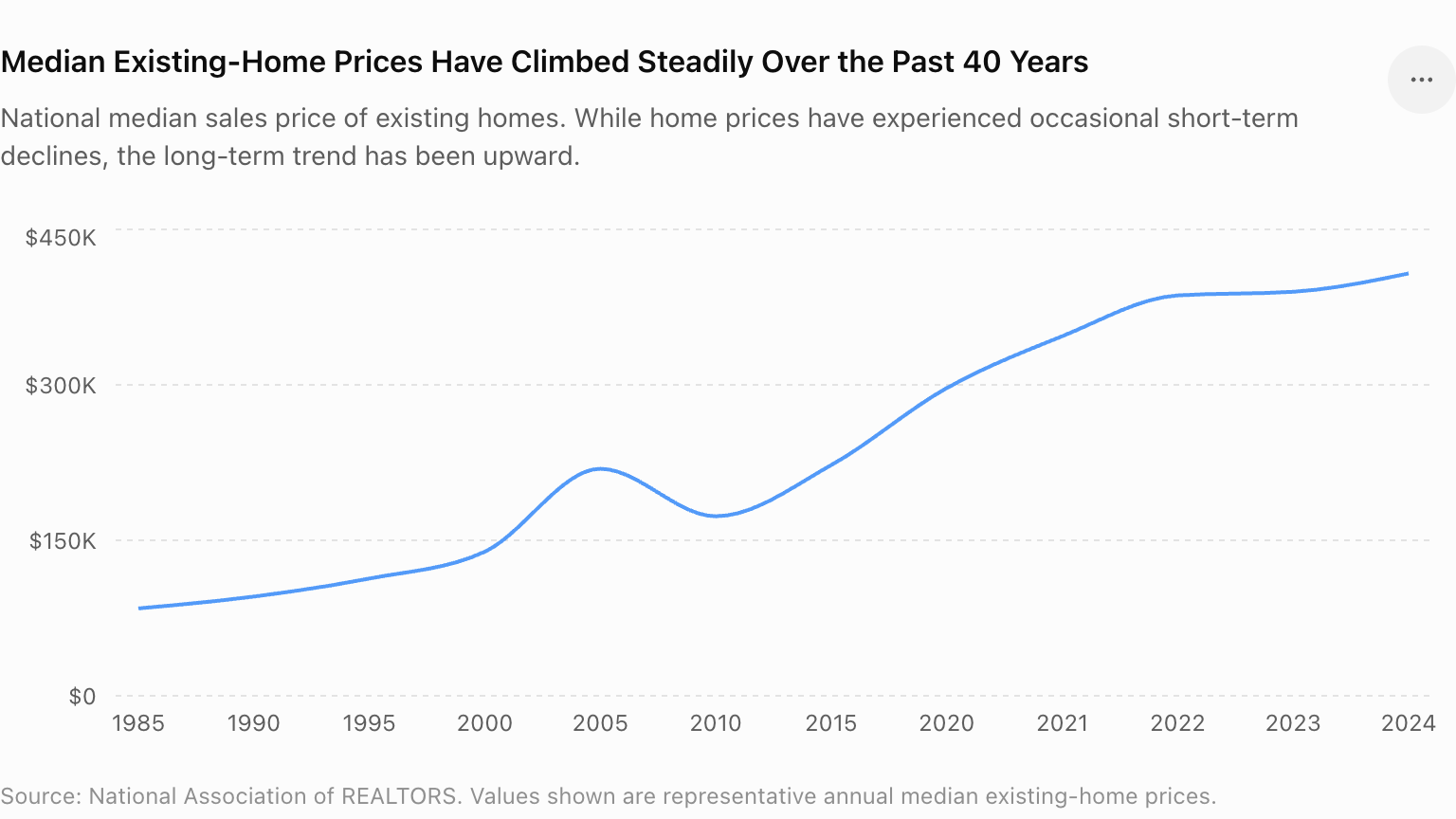

Home values, on the other hand, have historically trended upward over time. While there can be short-term fluctuations, real estate has consistently appreciated over the long run.

While mortgage rates have fluctuated dramatically over the past 60 years, ranging from historic lows below 3% to highs above 18%, home values have generally continued to rise over time. In fact, as the median home values shown above demonstrate, home prices have trended steadily upward across generations. That’s an important distinction because a lower rate tomorrow doesn’t necessarily offset a higher home price later.

A Real-World St. Louis Example

Let’s look at what this might have looked like for a typical first-time homebuyer in the St. Louis area.

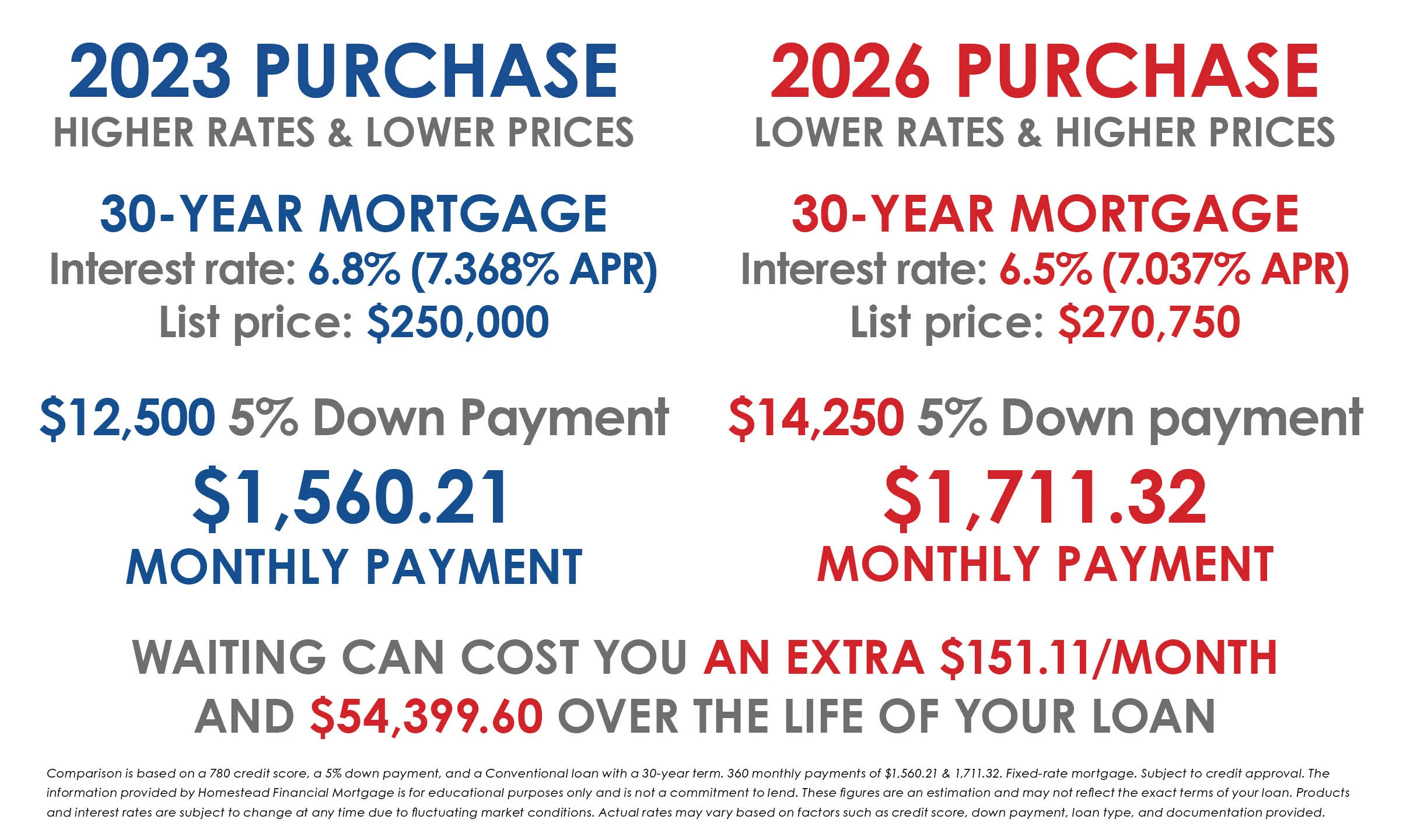

In 2023, the median home price in the St. Louis metro area was around $250,000.

Imagine you found the perfect home in 2023 for that price.

Buying in 2023

- Home Price: $250,000

- Down Payment (5%): $12,500

- Loan Amount: $237,500

- Average Mortgage Rate: Approximately 6.8% (7.368% APR)

Your estimated principal and interest payment would have been about $1,560.21 per month.

At the time, you may have looked at that interest rate & payment and thought: “Maybe I’ll wait for rates to come down.”

But let’s see what happened next.

What If You Waited Until 2026?

Fast forward three years…

Mortgage rates have improved slightly and are now around 6.5%.

That sounds like good news.

However, home prices have continued to rise.

That same $250,000 home from 2023 is now worth approximately $285,000.

If you decide to buy that home today:

- Home Price: $285,000

- Down Payment (5%): $14,250

- Loan Amount: $270,750

- Mortgage Rate: Approximately 6.5% (7.037% APR)

Your estimated principal and interest payment would now be about $1,711.32 per month.

Even though the interest rate is lower, your monthly payment is actually higher because you’re financing a much more expensive home. And it can cost you extra over the life of your loan.

The Hidden Cost of Waiting

When you compare the two buyers, the difference becomes clear. The buyer who purchased in 2023 locked in a $250,000 purchase price and began building equity right away through their monthly mortgage payments. As home values increased, they also benefited from approximately $35,000 in appreciation, while still having the option to refinance later if rates fall.

The buyer who waited until 2026 is in a very different position. That same home may now cost around $285,000, which means a larger down payment, a higher loan balance, and a higher overall cost to purchase the same property. They also missed out on several years of equity growth that the 2023 buyer may have already gained.

The buyer who purchased in 2023 didn’t just secure a home. They secured a lower purchase price, and that’s something you can’t go back and get later.

You can refinance your interest rate, but you can’t refinance your purchase price.

That’s why many mortgage professionals encourage buyers to focus less on trying to perfectly time interest rates and more on purchasing when they’re financially ready and have found the right home. While nobody can predict exactly where rates will go next, history has shown that homeownership rewards those who spend time in the market rather than those who spend years waiting for the perfect moment to buy.

Start Building Equity Sooner

For every month you own a home, you’re building equity in an asset that may increase in value over time. The buyer who purchased in 2023 has spent the last three years building wealth through homeownership while benefiting from rising home values. The buyer who waited, on the other hand, missed out on years of equity growth. And if they were renting during that time, their monthly payments helped pay down someone else’s mortgage rather than building ownership in a home of their own.

The Bottom Line

Waiting for mortgage rates to drop may seem like a smart strategy, but it’s important to consider the full picture.

A slightly lower rate doesn’t always offset years of home price appreciation, and real estate is one of the smartest investments you can make.

Buying now allows you to:

- Lock in today’s home prices

- Start building equity immediately

- Benefit from future appreciation

- Refinance later if rates improve

- Invest in your long-term financial future

At the end of the day, the best time to buy isn’t necessarily when rates are lowest. It’s when you’re financially ready to become a homeowner. If you are wondering if you’re ready and what you can afford, now is the time to consult one of our loan advisors. We have strategies that can help lower your down payment and even help you buy a multi-unit property that can generate extra income to pay down your mortgage faster.

Reach out today to see if you’re ready to buy and begin your homeownership journey.