And Other Reasons Why Waiting to Buy Real Estate Is a Bad Idea

Jayson Hardie – Managing Partner – (636) 256-5712

Jayson Hardie – Managing Partner – (636) 256-5712

Thinking about waiting to buy a home? Let’s take a walk through the numbers—and history—to show why that might not be the smartest move. Yes, again.

We’ve already made the case with demographics (and why the age of a first-time buyer is rising) and supply vs. demand (spoiler alert: not enough homes, still). But this time, we’re going historical. Like, Federal Reserve data since 1963 historical.

A common excuse for waiting:

“Home prices have gone up so fast, they have to come down.”

Sure, gravity works on apples. But home prices? Not so much. So, before you start quoting Newton saying that what goes up MUST come down, remember: Isaac Newton was a brilliant physicist—but let’s face it, he’d make a pretty lousy real estate agent.

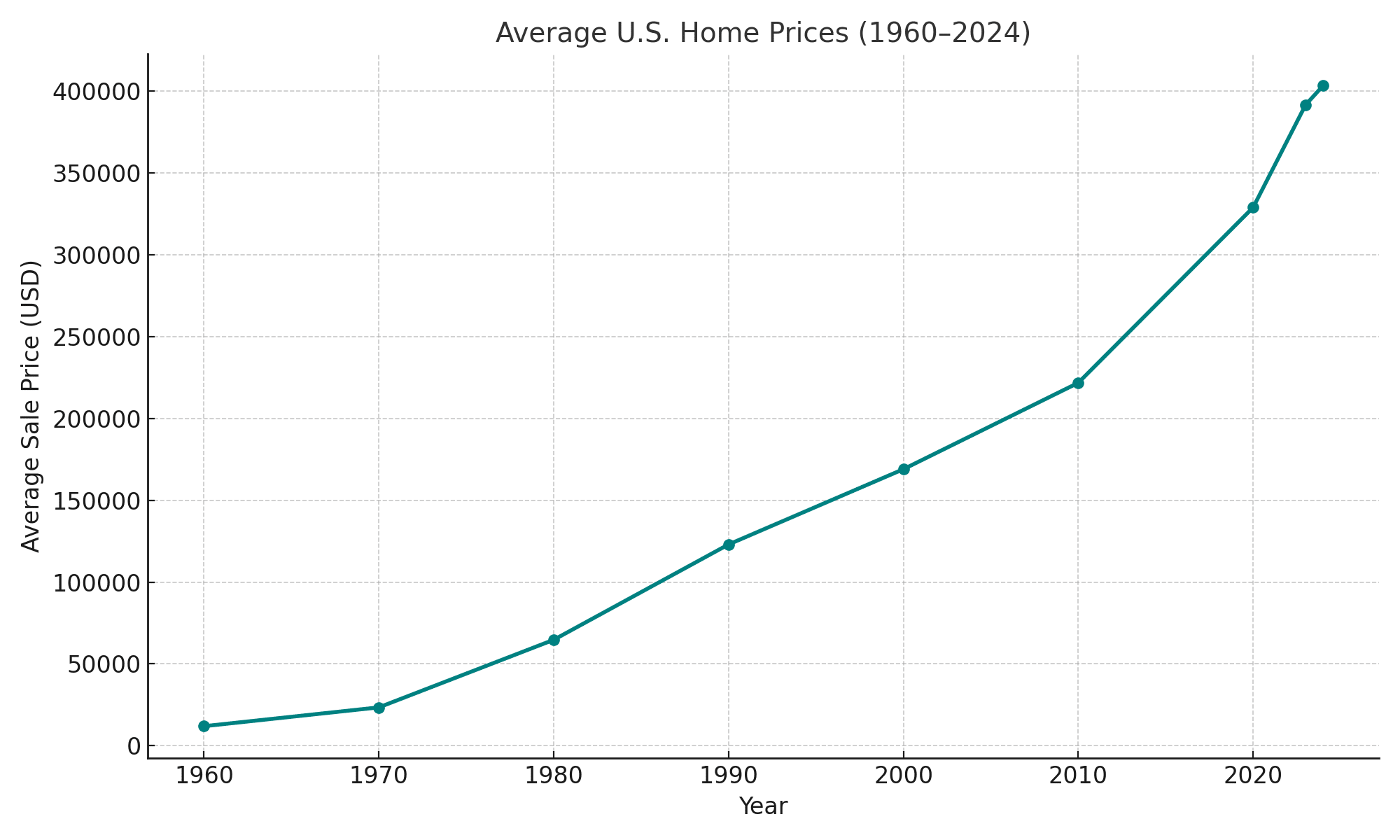

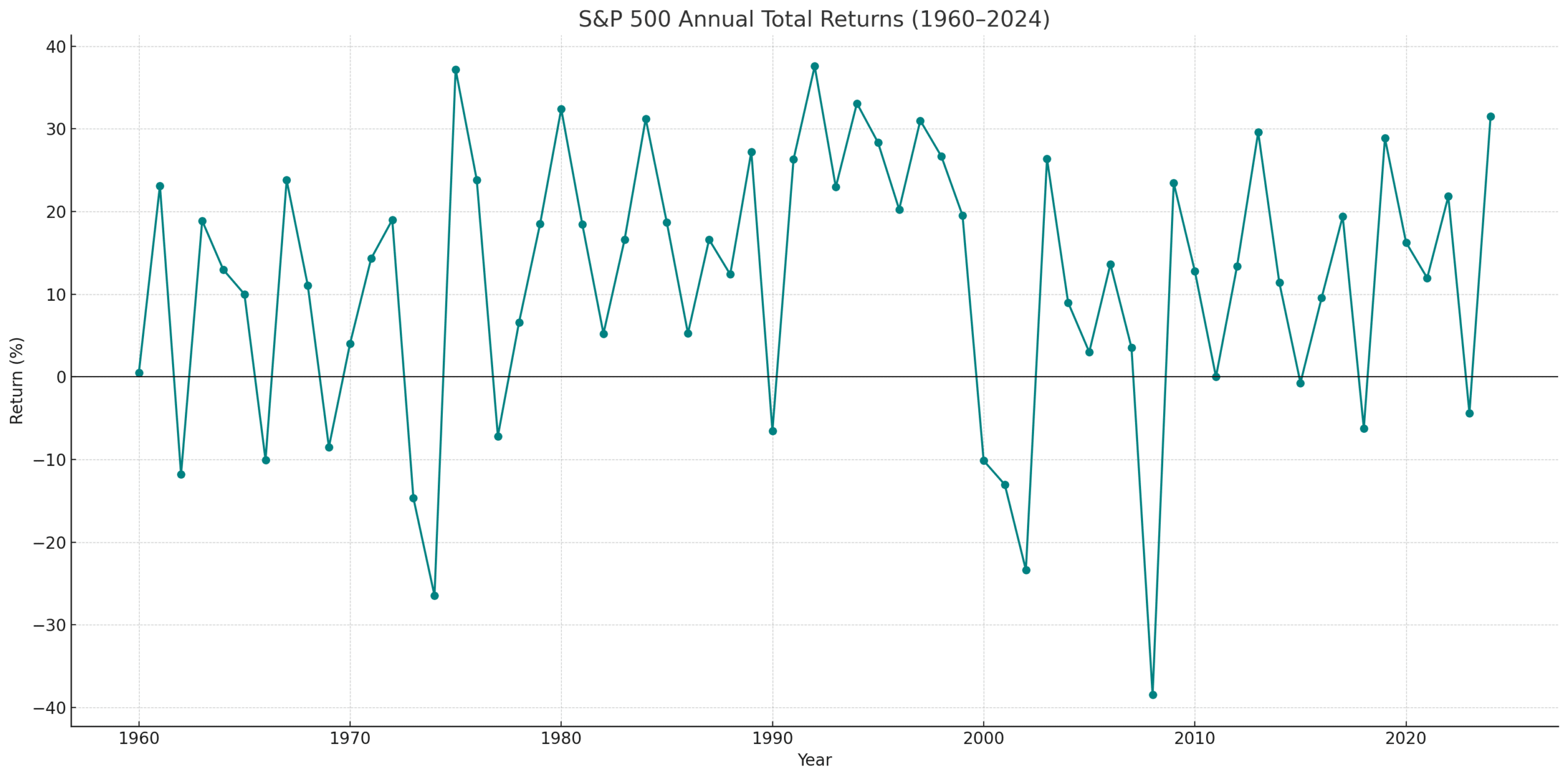

Let’s take a look at how real estate has performed over the decades compared to the S&P 500:

Here’s what the data tells us:

| Metric | Real Estate | S&P 500 |

| Years with losses > 1% | 5 | 13 |

| Worst 1-year loss | -10.9% (2009) | -37.0% (2008) |

| Average annual return | 5.5% | 11.71% |

How Real Estate Has Performed Over the Years

Real estate has historically shown impressive resilience. Over the past 60+ years, it’s only posted significant annual losses (more than 1%) five times. Compare that with the S&P 500, which has had thirteen such years, more than double. Even during major economic events, like the 2008 financial crisis, real estate bounced back more steadily than the stock market. After its worst year in 2009 with a -10.9% decline, home values began recovering and have since reached new highs.

What’s more, the long-term growth of real estate has been steady and reliable. A 5.5% average annual return might not sound flashy next to the S&P’s 11.71%, but real estate’s strength lies in its consistency. It doesn’t swing wildly with market emotions, tweets, or tech earnings. It grows. Slowly. Surely. Predictably.

And let’s not forget the power of leverage. Most people don’t buy homes with 100% cash—they use a mortgage. That means even modest appreciation can yield significant returns on your actual investment. Add in the tax advantages, rental income potential, and the fact that you’re living in the asset while it appreciates, and the case gets even stronger.

What This Means for You

Yes, the S&P 500 delivers higher returns on average. But it’s also way more volatile. Real estate, on the other hand, is a steadier ride—fewer dips, fewer freak-outs, and you don’t need a stomach of steel to stay invested.

And here’s the thing: you’ve got to live somewhere—whether you own it or not. So why not make your home work for you, rather than your landlord? Every rent check you write is helping someone else build equity and grow their wealth. Wouldn’t it make more sense if that someone were you? When you buy a home, you’re not just getting a place to live; you’re investing in an asset that historically grows in value over time. It’s like paying yourself instead of a landlord. So, if you’re going to be making monthly payments anyway, why not let those payments go toward something you actually own?

If you’re banking on a big crash in home prices, history isn’t really on your side. Real estate corrections happen, but deep declines are rare and short-lived compared to the stock market.

The Bottom Line

Newton’s laws work great in physics class. But real estate doesn’t obey gravity the way falling apples do. Waiting for prices to “come down” might just mean watching them go even higher while you’re on the sidelines.

In other words: Don’t be Newton. Be a homeowner.